Space-Tech Roundup + Update: Q2' 2024

SpaceTech Funding Rockets to $3.3 Billion in Q2 2024 Despite Economic Headwinds, Debt and Global Competition Rise, Funding Shifts Toward Maturity & More.

Welcome to Savant In Space! This is Abhinav, here to unlock and share some of the funding trends that we are noticing in the SpaceTech sector. The link to my brief report is at the bottom of the page!

A. Investment Growth + Trends

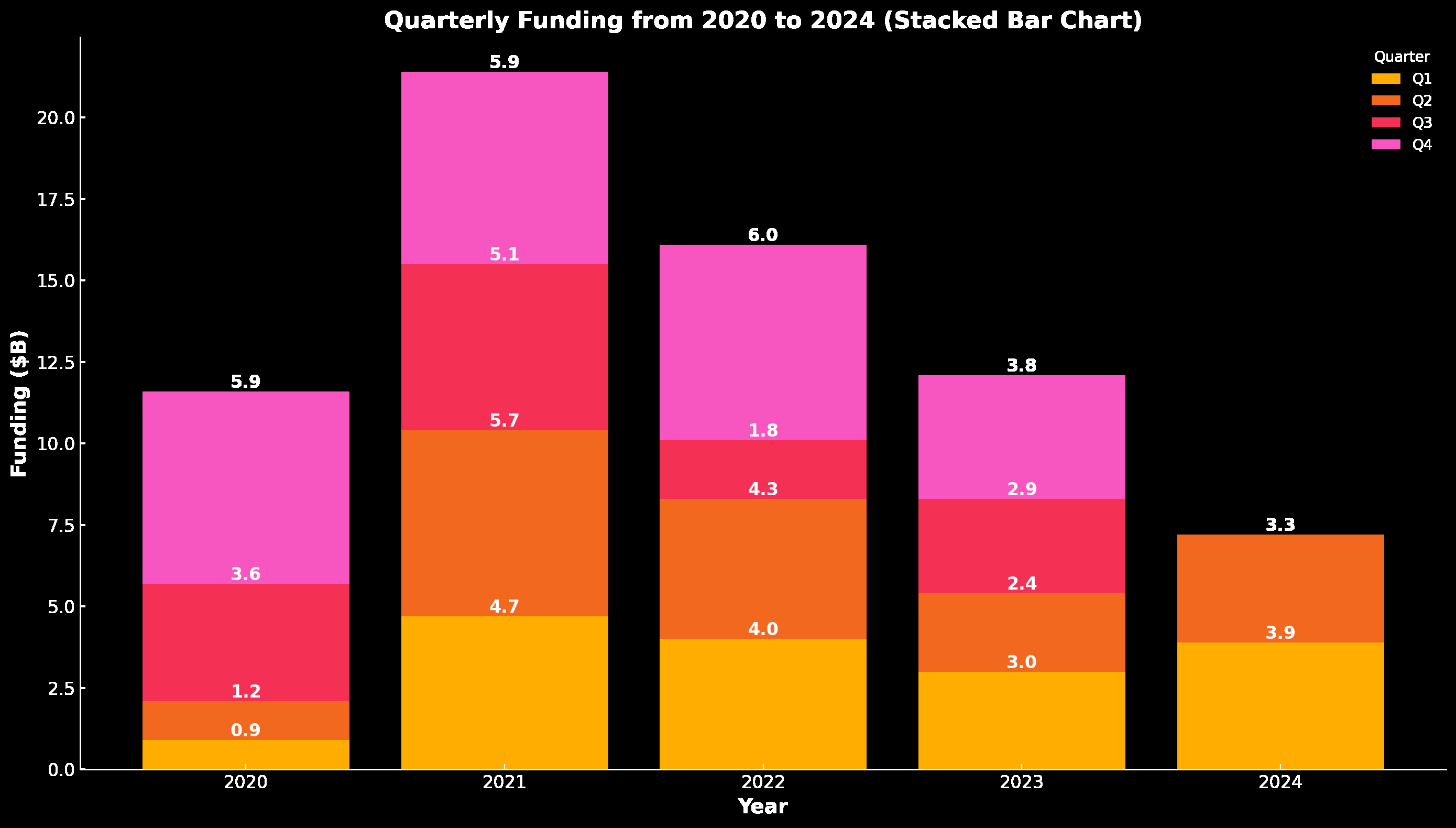

Alright, let's get down to brass tacks and examine the overall investment landscape. In Q2 2024, the space sector attracted a respectable $3.3 billion in private investment. While that's a healthy chunk of change, it does represent a dip from the $3.9 billion we saw in Q1 of the year. However, before you start sounding any alarm bells, remember that this still marks a significant 36% jump compared to Q2 of 2023!

So, what's behind this slight slowdown? Well, the global economy is definitely playing a role. Rising interest rates and persistent inflation are making investors a bit more cautious. But here's the thing – the space sector is proving to be far more resilient than many anticipated.

Here's a quick historical snapshot:

2023: A bit of a sleepy year for space investment, totaling around $12 billion – a noticeable decline from the exuberance of previous years.

Q1 2024: A strong start to the year, with that $3.9 billion figure signaling renewed optimism.

Q2 2024: While down from Q1, the $3.3 billion invested still demonstrates sustained momentum.

What's particularly interesting is the growing role of debt financing. In Q2, debt accounted for a substantial portion of the overall investment, signaling a potential shift in how space companies are accessing capital. We'll dig into that a bit more later on.

Zooming In: Okay, so we've got a good grasp on the overall investment picture. Now let's zoom in and explore some of the finer details, see where the money is flowing, and what that tells us about the sector's priorities.

🧱 Infrastructure Investment is Strong: First off, it's clear that Infrastructure remains the king of the hill. In Q2, it gobbled up a whopping $2.1 billion – that's over 60% of the total investment pie! And this isn't a new trend; Infrastructure has consistently pulled in over $10 billion annually since 2020. Think about it – launch vehicles, satellites, ground stations – these are the foundational building blocks of the space economy.

🚀 Satellite Manufacturing Startups are attractive: But within Infrastructure, there are some fascinating nuances. Satellite Manufacturing is absolutely booming, with companies like MinoSpace (CN) and Astroscale (JP) raking in major funding rounds thus far. And Heavy Launch isn't far behind. After all, you need those powerful rockets to get those shiny new satellites into orbit!

🌍 Applications: Now, let's turn our attention to Applications. This segment saw a nice little rebound in Q2, attracting $1.8 billion – that's more than the entire year of 2023! This tells us that investors are starting to see real potential in companies that leverage space data to solve real-world problems here on Earth. But hold on a second. There are some challenges brewing in Applications land. Remember that "growth-at-any-cost" mentality that fueled some of the hype in previous years? Well, investors are getting a bit more discerning now. They want to see clear paths to profitability and sustainable business models.

♻️ Emerging Industries: This is where things get really exciting, even though the industry is pretty nascent! On-Orbit Servicing, Space Situational Awareness – these are the frontiers of the space economy. While investment here is still relatively small compared to Infrastructure and Applications, we're seeing a steady stream of activity. Companies like Privateer Space (with its SSA focus) and D-Orbit (tackling On-Orbit Servicing) are paving the way for a more sustainable and dynamic space ecosystem.

🌎 Geographical: Okay, one more thing before we move on. Let's talk geography. The Americas still dominate the investment landscape, pulling in about 50% of the global total. But EMEA and APAC are stepping up their game, with China leading the charge in Asia. It's a truly global space race!

B. Segments

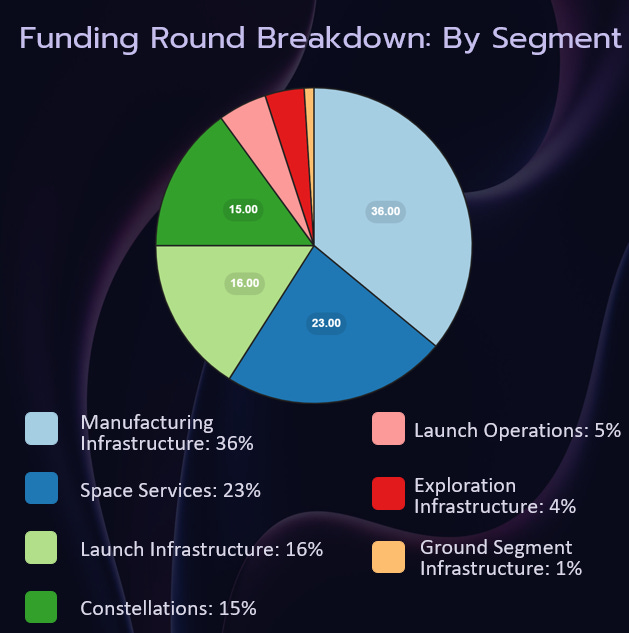

Manufacturing Infrastructure Reigns Supreme: A whopping 36% of funding rounds went to companies building the tools and technologies to produce satellites and related space hardware. This clearly signals that investors are betting heavily on the need to increase production capacity to meet the surging demand for constellations and other space-based assets.

Space Services on the Rise: Coming in second at 23%, Space Services captures a significant chunk of investment. This broad category likely includes companies involved in activities like satellite operation, data analytics, ground station services, and other downstream applications. It highlights the growing focus on utilizing space-derived data and infrastructure to create value here on Earth.

Launch Infrastructure Follows Closely: Securing 16% of the funding, Launch Infrastructure encompasses companies developing launch vehicles, launch sites, and supporting technologies. This segment's significance underscores the critical role of reliable and affordable access to space in fueling the entire space economy.

Constellations Gaining Momentum: Capturing 15% of the funding, companies building constellations – networks of satellites for communication, Earth observation, or other applications – are attracting significant attention. This highlights the growing interest in large-scale, space-based infrastructure and the potential of constellations to disrupt existing industries.

Constellations Drive Manufacturing and Launch: The pursuit of large constellations is directly fueling the demand for both Manufacturing Infrastructure (to build the satellites) and Launch Infrastructure (to deploy them). These segments are interconnected, and their growth trajectories are likely to be closely intertwined.

Space Services: Leveraging Infrastructure: The growth of Space Services is closely linked to the development of robust Infrastructure (launch and satellites). As access to space becomes more affordable and reliable, we can expect a flourishing of new Space Services that leverage these capabilities to deliver innovative solutions to terrestrial markets.

What Investors ought to focus on:

‘Supply Chain Dominance’: Investing in Manufacturing Infrastructure provides an opportunity to gain a strategic position in the space supply chain, potentially capturing value from the growth of constellations and other space hardware demand.

Downstream Value Creation: Investing in Space Services offers the potential for higher-margin returns as companies leverage existing infrastructure (launch and satellites) to develop value-added services and address specific market needs.

Picking Winners in the Launch Race: The Launch Infrastructure sector remains a key area of innovation and competition. Identifying launch providers with disruptive technologies, reliable track records, and sustainable business models is crucial for capitalizing on the growth of the launch market.

C. The Dealmaking

Alright, so we've dissected the investment trends – now let's talk about those big, splashy M&A deals! Q2 2024 was a whirlwind of acquisitions, with 11 deals announced. That's a serious uptick compared to the more subdued M&A activity we've seen in recent times. It seems like everyone's looking to partner up, consolidate, and strengthen their position in a rapidly evolving market.

The Big Deal: And speaking of big deals, let's talk about the elephant in the room: SES and Intelsat. This $5 billion mega-merger sent shockwaves through the industry. Two giants joining forces – it's a clear sign of consolidation in the satellite operator world. SES, with its strong multi-orbit strategy, is clearly looking to expand its reach and bolster its offerings. And Intelsat, facing some financial headwinds, gets a lifeline and a chance to be part of something bigger. It'll be fascinating to see how this plays out in the long run. While many believe that the deal is a response to the recent wave of consolidations we saw amongst what I refer to as “satellite-primes”, but there are certain aspects that one should not miss out on whilst looking at the SES <> Intelsat merger:

Consolidation Amidst Competition: The satellite industry is facing a classic squeeze. On one hand, demand for bandwidth and connectivity is skyrocketing, driven by everything from streaming services to the Internet of Things. On the other hand, competition is fierce, with new entrants like SpaceX's Starlink and Amazon's Kuiper aggressively challenging the established players. Consolidation becomes a survival tactic, allowing companies to pool resources, achieve economies of scale, and offer more comprehensive solutions.

Multi-Orbit Dominance: SES has been a vocal proponent of a multi-orbit strategy, recognizing that different orbits (GEO, MEO, LEO) offer distinct advantages for various applications. By acquiring Intelsat, SES gains a broader portfolio of satellites across multiple orbits, strengthening its ability to serve diverse customer needs and potentially offering more resilient and flexible services.

Expanding Reach, Diversifying Revenue: Intelsat brings a strong presence in government and mobility markets, complementing SES's focus on video broadcasting and data services. This diversification reduces reliance on any single market segment and creates opportunities for cross-selling and new revenue streams.

Technological Synergy: While details are still emerging, the merger likely presents opportunities to leverage each company's technological expertise. SES has invested heavily in next-generation satellite technologies, while Intelsat brings extensive experience in ground infrastructure and network management. The combined entity could accelerate innovation and bring new solutions to market faster.

What drove this from organizational POVs?

Financial Pressures on Intelsat: Intelsat has been struggling financially, burdened by debt and facing challenges in a rapidly changing market. The merger provides a much-needed financial lifeline and allows Intelsat to restructure its debt under the umbrella of a more stable entity.

Strategic Imperative for SES: For SES, the merger is a bold strategic move to solidify its position as a leading global satellite operator. It's about proactively shaping the future of the industry, rather than reacting to the competitive pressures from new entrants.

Investor Appetite for Consolidation: The broader investment community has been signaling a preference for consolidation in the satellite sector, as evidenced by the recent flurry of M&A activity. This creates a favorable environment for deals like the SES-Intelsat merger.

But hey, it wasn't just about the mega-deals. We also saw some interesting acquisitions in the Emerging Industries space. Remember Privateer Space, that cool SSA startup founded by Apple co-founder Steve Wozniak? Well, they scooped up Orbital Insight, an EO analytics company, to boost their capabilities in the SSA market. It's a smart move that gives Privateer a broader range of data and insights to play with.

And then there's Aerospacelab, the satellite manufacturer, acquiring AMOS, an opto-mechanical systems provider. It's all about vertical integration, baby! By bringing more of the supply chain in-house, Aerospacelab can boost efficiency and potentially lower costs.

So, what's driving all this M&A activity? Well, a few things come to mind. First off, the rising interest rates we talked about earlier are definitely putting pressure on smaller companies. Merging with a larger player can provide much-needed financial stability and access to capital.

Secondly, competition is heating up across the board. Whether it's in launch services, satellite manufacturing, or downstream applications, companies are feeling the squeeze. By joining forces, they can pool resources, expand their offerings, and gain a competitive edge.

And finally, let's not forget about the ever-present drive for innovation. Acquiring a company with cutting-edge technology or a unique skillset can be a faster and more efficient way to innovate than building everything from scratch.

D. Major Funding Rounds

[Look at Jeff Bezos's unwavering commitment to Blue Origin through his substantial self-investment into Blue Origin]

Telesat ($1600M): Telesat secured this debt from the Canadian govt likely for its ambitious Lightspeed project - a LEO constellation aimed at providing global broadband internet access. This reflects the increasing government support for space-based infrastructure and Telesat's credibility as a major player in the SatCom market.

Blue Origin ($500M): Jeff Bezos's space venture secured a self-capitalization round, indicating Bezos's unwavering commitment to building a long-term presence in space. Blue Origin is competing on multiple fronts, from launch services (New Glenn rocket) to lunar landers and space tourism. This massive infusion of capital likely fuels further development and ambitious expansion plans.

Space Pioneer ($210M): One of the Chinese companies that is rapidly becoming a key player in the launch services market, focusing on affordable and reliable launch solutions. The $210 million Series C funding suggests significant investor confidence in their technology and growth potential, potentially positioning them as a major competitor to established players.

MinoSpace ($140M): MinoSpace specializes in Satellite Manufacturing, likely riding the wave of demand for constellation deployments (there were recent reports of China wanting to scale up their sat manufacturing and launch capabilities significantly).

ICEYE ($93M): It is already a leader in Synthetic Aperture Radar (SAR) satellite technology, aiming to provide high-resolution Earth observation data regardless of weather conditions.

PLD Space ($84M): Focused on small-satellite launch services, trying to fill a niche in the rapidly growing launch market. This funding round likely enables PLD Space to advance the development and testing of their launch vehicles, potentially making space more accessible to a broader range of actors and tapping into the European market, which is increasingly turning inward.

Isar Aerospace ($70M): Another contender in the small-satellite launch market, emphasizing low-cost and flexible launch solutions. The funding likely allows Isar Aerospace to refine their technology and compete in a market increasingly crowded with new launch providers.

X-BOW ($60M): A rather new entrant from Germany, that specializes in propulsion systems for small satellites. Their advanced propulsion technology is focused on maneuvering, de-orbiting, and extending the life of small satellites in orbit.

Privateer Space ($57M): [Proof that every billionaire wants to go to space!] This Steve Wozniak-backed venture focuses on Space Situational Awareness (SSA) and space debris mitigation, a critical need as orbital congestion grows. They also acquired Orbital Insight (see deals section).

E. Governmental Contracts

It's no secret that government initiatives and contracts play a massive role in shaping the industry's trajectory. And Q2 2024 was no exception. We saw some major moves from governments around the world, signaling a continued commitment to space exploration, technology development, and economic growth. 🌎🚀

First up, let's head over to Japan, where the government launched a massive $6.4 billion Space Strategy Fund. That's not a typo – billion with a "B"! This 10-year initiative, managed by JAXA, aims to pump serious capital into space businesses and R&D. They're laser-focused on supporting private companies and universities in developing cutting-edge technologies across space transportation, satellites, and exploration. It's a clear signal that Japan is serious about becoming a major player in the global space economy.

Meanwhile, South Korea is also making big moves. They just launched the Korea Aerospace Administration (KASA), a new agency that aims to unify and strengthen the country's space efforts. With an annual budget of $556 million and growing, KASA has its sights set on some ambitious goals, including space exploration, transportation, industry development, and even space security.

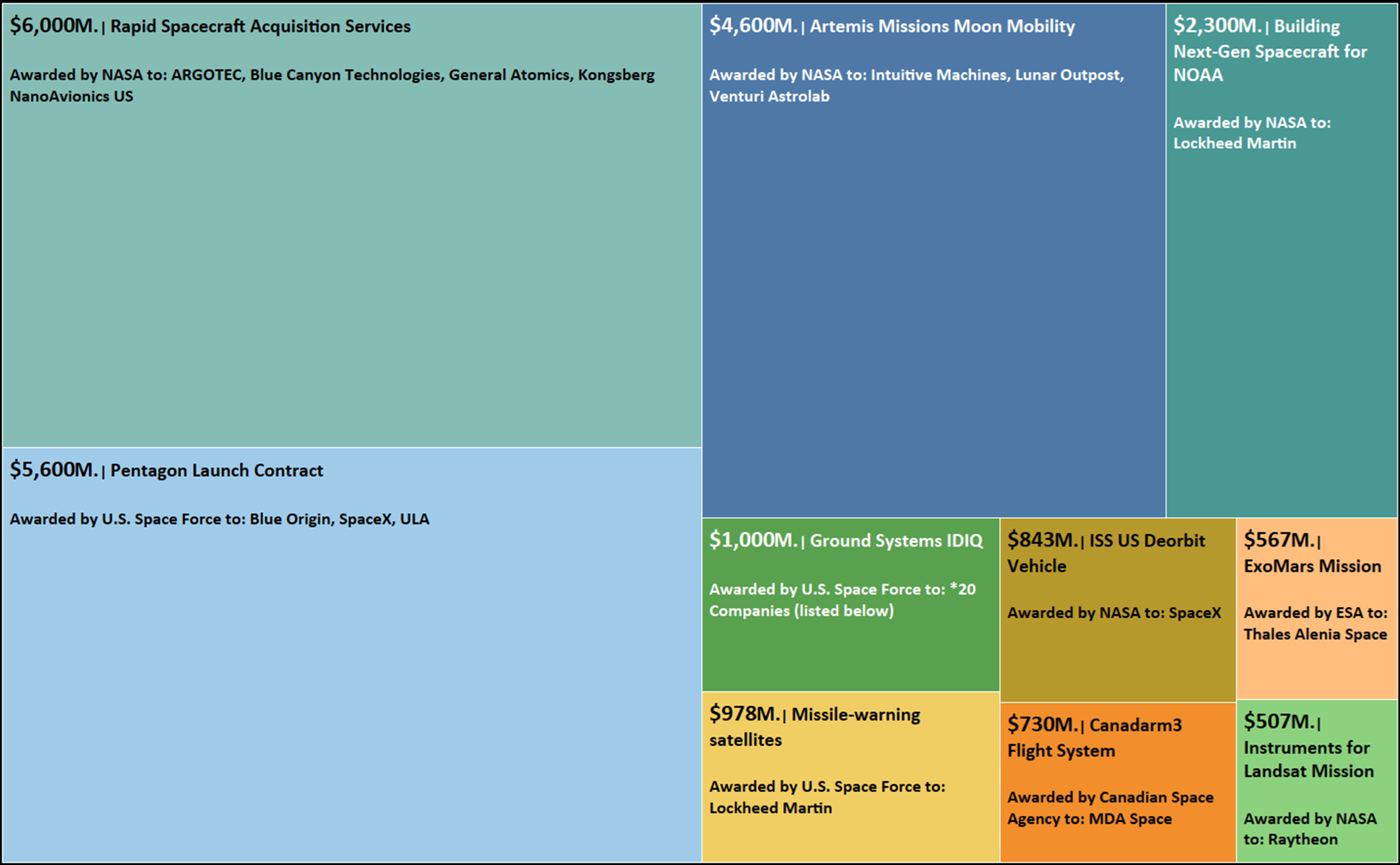

And of course, we can't forget about the big kahuna – NASA. In Q2, they awarded a staggering $6 billion in contracts for Rapid Spacecraft Acquisition Services (Rapid IV). This program is all about streamlining the process of acquiring satellites and spacecraft, ensuring that NASA has the tools it needs to carry out its missions. It's a huge boost for companies like ARGOTEC, Blue Canyon Technologies, and Kongsberg NanoAvionics, who snagged those coveted contracts.

But wait, there's more! NASA also doled out $4.6 billion for the development of Lunar Terrain Vehicles (LTVs) for the Artemis missions. Think lunar rovers, but way cooler. This is a major win for companies like Intuitive Machines, Lunar Outpost, and Venturi Astrolab, who are leading the charge in lunar mobility.

And speaking of Artemis, let's not forget about the U.S. Space Force. They awarded a hefty $5.6 billion in contracts for National Security Space Launch Phase 3. This program is all about ensuring that the U.S. military has reliable access to space for critical national security payloads. Blue Origin, SpaceX, and ULA are the big winners here, securing contracts that will keep them busy launching those top-secret satellites for years to come. 🤫

Okay, so what does all this mean? Well, first off, it's clear that governments are recognizing the strategic importance of space (from both a commercial, say public benefit POV as well as for defense). It's not just about exploration & scientific outcomes at this point – it's about economic competitiveness, national security, and technological advancement. Secondly, these initiatives and contracts provide a massive injection of capital into the space sector, kind of like trickle-down economics. This funding fuels innovation, supports the development of new technologies, and creates opportunities for both established players and startups.

And finally, it's a sign of growing collaboration between governments and private companies. We're seeing increasing adoption of public-private partnership (PPP) models, with governments leveraging the agility and innovation of the private sector to achieve their space goals & focusing more on setting the right policies and larger-level goals/vision.

F. IPOs and Exits

As any seasoned space investor knows, the journey to a successful exit is often as complex and challenging as a deep-space mission itself. It requires careful planning, precise execution, navigation and, well, a bit of cosmic luck. So let's examine the exit trends we've observed and explore what they tell us about the future of space-tech investment. 🌌

First, let's look at the IPO landscape. Q2 2024 saw one notable debut: Astroscale, the Japanese space debris removal company, went public on the Tokyo Stock Exchange, achieving a valuation of approx. $934 million. While this is a positive sign, it's worth noting that public markets have been less than welcoming to space companies in recent years. High growth expectations, coupled with the inherent risks and capital-intensive nature of the space industry, have made it tough for some companies to meet those lofty market expectations. Not to forget the SPAC-boom that has destroyed a lot of legitimacy for the sector.

On the acquisition front, Q2 was bustling with activity. There are also some potentially high-value deals expected to close in the latter half of 2024 and 2025. That was driven primarily by two Emerging Industries companies – indicating that even in this nascent space, strategic acquisitions are heating up.

There is a divergent approach between the Infrastructure segment and the Application segment.

But a deeper dive into the numbers reveals some interesting patterns. Over the past decade, acquisitions have accounted for a whopping 87% of infrastructure exit value. This suggests that for companies building the foundational elements of the space economy – launch vehicles, satellites, ground stations – getting acquired by a larger player is often the most viable path to a successful exit.

However, the path for Applications companies looks quite different. They've historically favored IPOs, often raising substantial capital to fuel global expansion and achieve those sought-after network effects. But as we discussed earlier, the growth-at-any-cost model is losing its luster. Investors are becoming more discerning, demanding clear paths to profitability and sustainable business models. This shift in investor sentiment could lead to a more balanced approach to exits, with a greater emphasis on strategic acquisitions and a focus on companies with proven revenue streams.

Looking ahead, the future of space-tech investment is likely to be shaped by a complex interplay of factors:

Macroeconomic conditions: Rising interest rates and economic uncertainty are likely to persist, making investors more selective and cautious.

Technological advancements: Breakthroughs in areas like reusable launch vehicles, advanced satellite technologies, and in-space manufacturing will continue to drive innovation and attract investment.

Government support: Continued investment and support from governments worldwide will be crucial for fostering growth and creating a favorable regulatory environment.

Moving ahead, successful space companies will need to be adaptable, resilient, and laser-focused on delivering real value – whether it's providing critical infrastructure, leveraging space data to solve Earthly problems, or pushing the boundaries of space exploration.

G. What Trends are Shaping This?

Trend 1: The Rise of Debt Financing and Its Implications

Deal analysis represents that there has been a significant rise in debt financing in Q2 2024, especially for infrastructure projects. For instance, the Telesat deal, securing a massive $1.6 billion in debt from the Canadian government, is not an anomaly but underscores the overall trend of increased debt participation.

This suggests a couple of things:

Maturing Industry: Lenders are becoming more comfortable with the space sector's long-term viability and predictable cash flows, especially for established operators like Telesat.

VC Pullback: The dip in traditional VC funding, partly due to macroeconomic factors, is pushing companies to seek alternative financing options like debt.

Potential Consequences: While debt can fuel growth, it also brings increased financial risk, especially if interest rates continue to rise. It will be crucial to monitor debt levels and ensure they are sustainable in the long run.

Trend 2: Geographic Shifts and Competition

Although there is continued dominance of the U.S. in terms of overall investment, it would be foolish to not note the growing activity in other regions. One specifically notes China's dominance in early-stage and growth-stage funding, surpassing the U.S. in the ‘Infrastructure’ segment.

This signals:

Global Space Race: Countries like China are aggressively investing in space technology, recognizing its strategic importance for economic competitiveness and national security.

Shifting Power Dynamics: The U.S. may face increased competition in the coming years, particularly in key areas like launch services and satellite manufacturing.

Trend 3: The Evolving Landscape of Applications

There are challenges facing Applications companies, particularly in terms of unit economics and achieving profitability. It seems that investor interest is waning in the "growth-at-any-cost" model, now replaced by the need for strong revenue growth to demonstrate viability.

Key Takeaways:

Consolidation is Likely: We might see more consolidation in the Applications space as companies struggle to achieve scale and profitability independently.

Focus on Sustainable Business Models: Investors are demanding a greater focus on revenue generation and sustainable business models, rather than just user growth.

Trend 4: The Disconnect Between Exits and Private Valuations

It is also obvious that there is some disparity between the high private valuations of some space companies and the more muted exit multiples we've seen in recent IPOs and acquisitions.

This suggests:

Market Correction: A potential market correction might be on the horizon, with private valuations adjusting to reflect the realities of the public markets.

Emphasis on Revenue & Profitability: Investors will be increasingly focused on companies with proven revenue streams and a clear path to profitability, leading to more rigorous due diligence and potentially lower valuations.

Trend 5: The Strategic Importance of Emerging Industries

There is, however, a growing interest in Emerging Industries, despite their relatively small share of overall investment. Q2 also marked several companies emerging from stealth mode in areas like On-Orbit Servicing, accentuated by the acquisition of Orbital Insight by Privateer Space in the SSA market.

This indicates:

Future Growth Potential: Investors recognize the long-term potential of Emerging Industries, even though they may not yet generate substantial revenues.

Strategic Acquisitions: Larger companies are looking to acquire startups with innovative technologies in these areas to gain a foothold in these emerging markets.

Trend 6: Data Transmission a Bottleneck? The limitations of downlinking massive amounts of data from space are implied by the focus on companies like Scale AI, which specializes in AI data infrastructure, and the overall growth of GEOINT applications.

Logic: Satellites are collecting more data than ever before, but transmitting that data back to Earth remains a significant bottleneck.

Bottleneck Breeds Opportunity: This creates a pressing need for innovative solutions in areas like ground station infrastructure, data compression, and edge computing in space.

H. Satellite Sub-Segment in Q2 ‘24

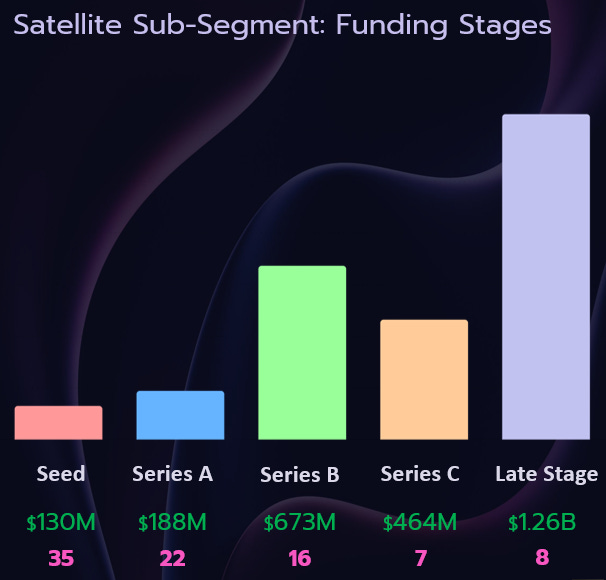

Late Stage Dominance? A whopping $1.26 billion was invested in late-stage satellite ventures, overshadowing all other funding stages. This indicates a Maturing Satellite Market (specially in the US where most SpaceTech seems to be geographically concentrated) as investors are favoring companies that have already proven their technology, demonstrated market traction, and are likely closer to generating significant revenue or achieving a successful exit (IPO or acquisition). Additionally, given the risk with attaining space qualification, flight heritage matters as evidenced by this, since later-stage companies often have the advantage of "flight heritage," meaning they've successfully launched and operated satellites in orbit. This significantly reduces perceived risk for investors.

Series B funding attracted a significant $673 million, the second-largest amount after late-stage. However, there were only 16 Series B deals compared to 35 seed deals and 22 Series A deals. This suggests a strong competition for growth capital. The competition for Series B funding is intense. Only the most promising companies with strong growth potential and compelling business models are able to secure these larger investments. It could also be the fact that investors are betting on companies that are closer to being profitable and have figured out the commercialization angle.

Want to Download the Report? You can download the report from here.